The announcement of reciprocal tariffs on 2 April 2025, alongside reactions from affected countries, stands as the most significant economic development globally that year.

Against this backdrop, it is crucial to assess the impact of the evolving trade environment on Cyprus’s export performance. During January-August, the value of exports of goods rose by 2.8%YoY, a notable slowdown compared to the robust 26.0%YoY growth in the same period of 2024.

The year’s increase slightly outpaces the EU’s average growth of 2.0%YoY, after a minor contraction of 1.5%YoY the year before. Thus, despite growth deceleration, Cyprus’s exports appear relatively resilient during the first eight months of 2025.

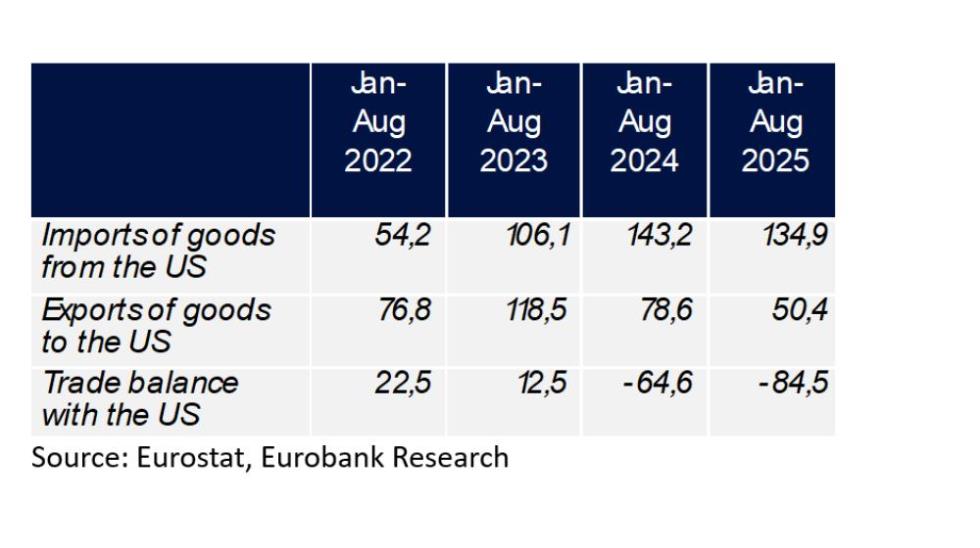

Regarding exports to the U.S., which are a small portion of Cyprus’s total goods exports (2.2% in 2015-2024), they experienced a significant decline in the January-August period, falling by 37%YoY, after a similar sharp drop of 33.7%YoY in the same period of 2024. The decline in both years is largely attributed to reduced exports of ships and aircraft and cannot be directly linked to tariff-related disruptions.

Consequently, the U.S. now accounts for just 1.4% of Cyprus’s total merchandise exports. The historically low dependence on U.S. demand, in combination with the upward trajectory in overall merchandise trade, mitigates the importance of the weakening in the U.S. share.

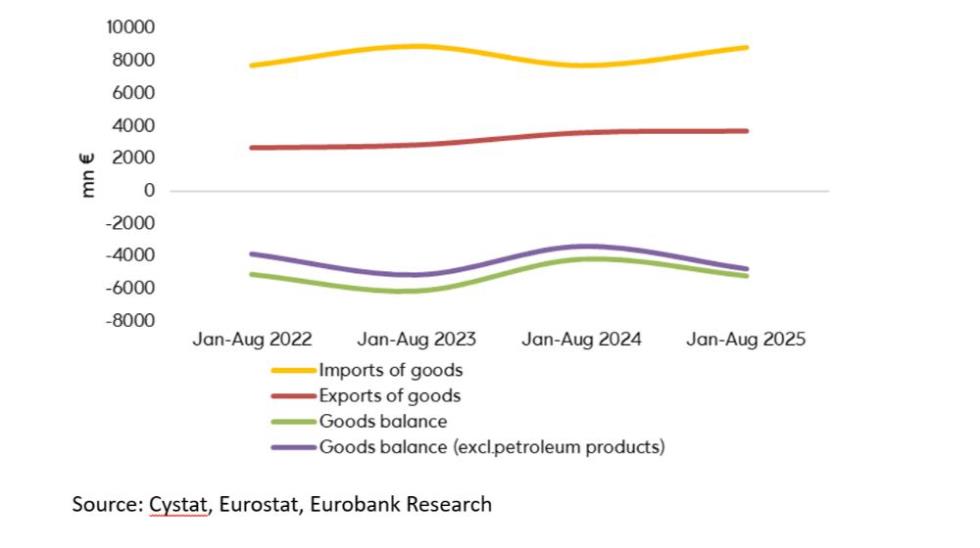

Focusing on the overall picture of goods exports in 2025, the 2.8% rise is almost entirely driven by a substantial surge in exports of petroleum products, by 281.9%. This sharp rise led to a dramatic increase in the share of petroleum products in Cyprus's total merchandise exports, from 16.3% in 2024 to 44.8% this year.

Excluding petroleum products, exports of goods have fallen by 32.1%YoY, reaching a four-year low of €2.06bn, almost entirely from a base effect, i.e. very high exports of ships in 2024, while total imports rose by 6.8%YoY, mainly due to higher imports of chemical products, motor vehicles and pharmaceuticals. The surge in petroleum exports, benefiting activity in the refineries industry, is likely tied to a revival of seaborne trade through the Red Sea route, with their imports rising by 51.3%YoY. However, the petroleum products deficit has narrowed by 45.9%YoY, while the overall merchandise trade deficit has worsened by 24.5%YoY, because of the mentioned idiosyncratic factors (reduced exports of ships, alongside increased imports of chemicals, vehicles).

*Michail Vassileiadis, Research Economist, Eurobank Group