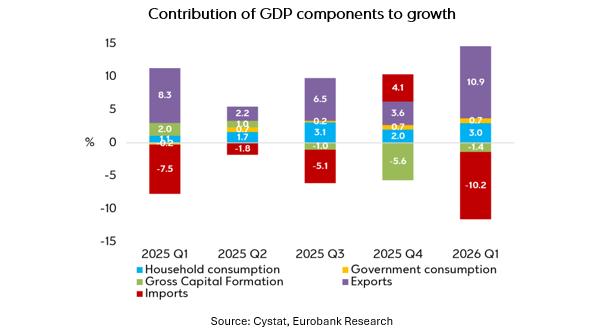

GDP growth decelerated to 3.0%YoY in Q1 2026 from 4.3%YoY in Q4 2025 and 3.6%YoY in Q1 2025, marking the weakest outturn in ten quarters.

Based on the expenditure breakdown, the slowdown was primarily driven by a less favourable contribution from net exports. Although both exports and imports expanded at a robust pace of 10.5%YoY and 10.4%YoY, respectively, this represented a marked deterioration relative to the previous quarter, when exports increased by 3.4%YoY while imports contracted by 3.9%YoY. The strong rebound in imports largely reflects base effects associated with low investment in transport equipment, including ships and aircrafts, recorded a year earlier.

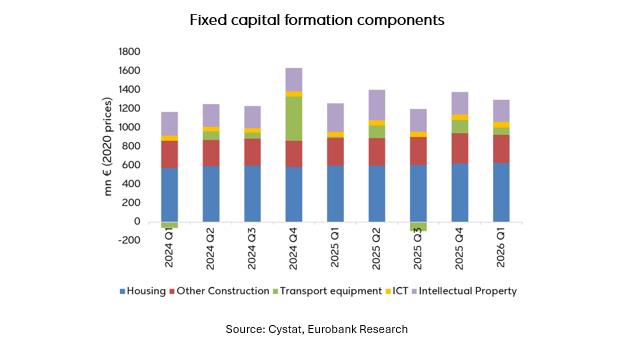

In contrast, domestic demand dynamics improved across components. Private consumption growth accelerated to 4.9%YoY, from 3.6%YoY in Q4 2025, supported by still-favourable labour market conditions, with unemployment declining to a Q1 record-low of 4.0%. Government consumption also accelerated mildly, expanding by 4.6%YoY, compared with 4.3%YoY in the previous quarter. Gross fixed capital formation contracted for a second consecutive quarter, but the pace of decline moderated significantly to 6.9%YoY, from 21.7%YoY in Q4, mainly reflecting the aforementioned transport-equipment-related base effects. Residential construction remained resilient, with housing investment expanding by 4.7%YoY, after 5.9%YoY in Q4, supported by strong mortgage lending growth of 23.1%YoY in 2025. By contrast, momentum weakened considerably in other construction works, where growth slowed to 0.8%YoY, from 17.5%YoY, while investment in intellectual property products, which had been among the fastest-growing capital categories in recent years, contracted sharply for a second consecutive quarter (-62.3%YoY following -70.1%YoY in Q4).

Contribution of GDP components to growth

Source: Cystat, Eurobank Research

Looking ahead, provided that the 60-day ceasefire agreement announced on June 17 contributes to a lasting de-escalation in the Persian Gulf and the broader Middle East region, the macroeconomic impact of the latest geopolitical crisis is expected to remain contained. Tourism and transport are likely to bear the brunt of the shock, weighing on services exports, while ICT, financial services and other business services should remain largely insulated.

After a record year for tourist arrivals in 2025 and a strong 9.1%YoY increase during the first two months of 2026, arrivals declined sharply by 28.6%YoY in March-April. Encouragingly, the pace of contraction eased substantially in May, to 4.9%YoY, raising the prospect of an -at least partial- recovery during the peak summer season. Nevertheless, any weakness in tourism-related activities could spill over into adjacent sectors, including logistics and retail trade, weighing on employment and household disposable income. Labour market indicators have already begun to reflect some pressures, with registered unemployment increasing by 9.0%YoY in April-May, reversing the 2.2%YoY decline recorded in Q1. The rise was concentrated in tourism, administrative services and logistics-related activities. Private consumption is also likely to face headwinds from higher inflation, which accelerated to 4.0%YoY in June (flash estimate) from 0.9%YoY in February, as the pass-through of higher energy costs increasingly feeds into services prices via second-round effects. These pressures should be partly mitigated by government measures aimed at containing imported inflation, as well as by a stronger wage indexation adjustment, which has increased to 90% since this July, from 66.5% in previous years. At the same time, a moderation in household consumption growth is likely to curb import demand, partly offsetting the impact of softer export performance on the external balance.

On the investment side, the strong contribution from construction activity is expected to remain broadly intact through the remainder of 2026. Building permits increased by 48.8%YoY in January-February, while the authorised construction area rose by an even stronger 56.5%YoY. The outlook is further supported by resilient real estate market activity, with property sales volume rising by 14.1%YoY in January-April, and housing credit growth accelerating to 24.5%YoY in Q1 2026, extending last year's robust expansion. However, property sales growth slowed markedly to 4.8%YoY in May, primarily reflecting weaker demand from foreign buyers. Growth in foreign transactions decelerated to 9.0%YoY from 21.1%YoY during the first four months of the year, while purchases by Cypriot residents slowed to 2.5%YoY from 9.3%YoY previously. Foreign buyers remained the principal driver of market activity during January-May, accounting for 61% of the increase in total sales, with approximately 60% of them originating from non-EU residents.

Overall, the macroeconomic environment remains supportive of investment, underpinned by strong public finances, continuously improving financing conditions, a business-friendly regulatory and tax framework, and Cyprus’s strategic geographic position. The main structural constraint on growth continues to be labour shortages, as reflected in the elevated vacancy rate of 2.8% in Q1 2026. Addressing these bottlenecks through policies that facilitate targeted labour mobility and attract foreign workers in selected areas of expertise will remain essential for sustaining the economy’s medium-term growth potential.

Fixed capital formation components