Would you rather have €1 million today—or a single cent that doubles every day for a month?

Let’s break that down. Dimitris chooses the €1 million today and Sophia chooses a single cent that doubles every day for a month.

- On Day 1, Dimitris has €1 million, while Sophia has €0.01. Pathetic.

- On Day 2, Dimitris has €1 million, while Sophia has €0.02. Still pathetic.

- On Day 5, Dimitris has €1 million, while Sophia has €0.16. Not even close.

- On Day 10, Dimitris has €1 million, while Sophia has €5.12.

- On Day 20, Dimitris has €1 million, while Sophia has €5,242.88.

- On Day 25, Dimitris has €1 million, while Sophia has €167,772.16.

- On Day 27, Sophia has €1,342,177.28 and overtakes Dimitris.

- On Day 30, Dimitris still has €1 million, while Sophia has €5,368,709.12.

This is the power of compound interest.

Let's start with the basics. When you put money in a savings account or invest it, you earn a return — typically expressed as an annual interest rate. There are two types of interest: simple and compounding.

Simple interest is straightforward: you earn a fixed percentage on your original sum every year. If you deposit €1,000 at 5% simple interest, you earn €50 per year. After 10 years, you have €1,500.

Compounding interest works differently — and far more powerfully. Instead of earning interest only on your original €1,000, you also earn interest on the interest you've already accumulated. After year one, you have €1,050. In year two, you earn 5% on €1,050 — not just on €1,000. That gives you €1,102.50. The next year, you earn on €1,102.50. And so on.

The difference sounds small at first. But over decades, it becomes extraordinary.

The Mathematics Behind the Magic

For those who appreciate the mechanics, here is the core formula:

FV=PV*(1+r/n)n*t

Where:

- FV = the future value of your investment

- PV = the principal (your initial amount)

- r = the annual interest rate (as a decimal, so 5% = 0.05)

- n = the number of times interest compounds per year

- t = the number of years

The key takeaway is that the future value of your investments is directly dependent on the:

- Initial amount you invest: can be constrained, especially in the early years of your career;

- Annual interest rate: not in your control;

- Number of times it compounds per year: again, not in your control;

- Number of years you hold the investment.

To make it tangible, consider two investors, Andreas and Maria, both 25 years old:

- Andreas invests €5,000 today and never adds another cent, at a 7% annual return.

- Maria waits 10 years, invests the same €5,000 at 35, and also earns 7%.

By age 65:

- Andreas's €5,000 grows to approximately €74,872.

- Maria's €5,000 grows to approximately €38,061.

Same amount invested. Same interest rate. A 10-year head start made Andreas nearly twice as wealthy. That is the power of time in compounding — and it is the single most important lesson in this article.

The Snowball on the Hill

A useful way to visualise compound interest is to imagine a snowball rolling down a hill. At the top, it's small. As it rolls, it picks up more snow. The bigger it gets, the more snow it collects with every rotation. By the bottom of the hill, what started as a handful of snow is now an enormous ball.

Your money behaves the same way. The longer the hill — meaning the longer your investment horizon — the bigger the snowball. This is why financial professionals universally agree: starting early is the single most powerful action a young investor can take.

Compounding Frequency: Why It Matters

Interest doesn't always compound once a year. It can compound:

- Annually — once per year;

- Quarterly — four times per year;

- Monthly — twelve times per year;

- Daily — 365 times per year.

The more frequently interest compounds, the faster your money grows. The difference between annual and daily compounding on a large sum over many years can amount to thousands of euros. When evaluating savings accounts or investment products, always ask: How often does this compound? That single question can meaningfully affect your outcome.

Compounding Works Against You Too

Here is the uncomfortable truth that most financial literacy discussions gloss over: compound interest is a double-edged sword.

If you are earning compound interest on an investment, it works beautifully in your favour. But if you are paying compound interest on debt — like a credit card balance, a personal loan, or a consumer overdraft — it works just as powerfully against you.

Consider a €3,000 credit card balance at an 18% annual interest rate, compounded monthly. If you make only minimum payments, that debt can take over 10 years to clear and cost you more than double the original sum in total interest payments.

This is why the same principle that builds wealth can destroy it. Understanding which side of compound interest, you are on is one of the most important financial habits you can develop.

As a general rule: eliminate high-interest debt first, then redirect those payments into compounding investments.

The Barriers: Why People Miss Out

If compound interest is so powerful, why doesn’t everyone take full advantage of it? The answer lies less in mathematics and more in human behavior.

- The difficulty of delayed gratification: compounding rewards patience—but people are naturally wired to prioritise the present over the future. Choosing to save or invest today often means giving up something tangible now for a benefit that feels distant and abstract. This trade-off is psychologically difficult, especially when the early gains from compounding appear small and insignificant.

- Underestimating exponential growth: human intuition is linear, not exponential. We tend to think in straight lines—expecting steady, incremental progress—while compound interest grows slowly at first and then accelerates rapidly over time. As a result, many people dismiss early investing efforts because the initial impact seems negligible, not realizing that the most significant growth happens later.

- The illusion of “starting later”: a common belief is that one can delay investing and simply contribute more later to “catch up.” While higher contributions do help, they rarely compensate for lost time. The early years of compounding are disproportionately valuable, and postponing them can significantly reduce long-term outcomes.

- Lifestyle inflation: as income increases, spending often rises alongside it. Instead of allocating additional earnings toward savings or investments, individuals may upgrade their lifestyle—larger homes, more frequent travel, or higher day-to-day expenses. This reduces the capital available to benefit from compounding.

- Interrupting the process: compounding works best when left uninterrupted. However, market volatility, short-term financial needs, or emotional decision-making can lead individuals to withdraw investments prematurely. Even temporary interruptions can materially reduce long-term results, particularly if they occur during periods of strong growth.

- Lack of financial literacy: finally, many people simply do not fully understand how compound interest works. Without a clear grasp of its long-term impact, it is easy to underestimate the importance of starting early, contributing consistently, and remaining invested.

Practical Vehicles for Compound Growth

In Cyprus and across Europe, young investors have access to several instruments where compounding works in their favour:

Savings Accounts & Term Deposits

The most accessible starting point. Cypriot banks offer savings and fixed-term deposit accounts. While interest rates have historically been modest, the current higher-rate environment across the Eurozone has made these more attractive. Always confirm the compounding frequency, fees and whether interest is reinvested automatically.

Investment Funds & ETFs

Exchange-traded funds (ETFs) and mutual funds that track broad market indices — like the MSCI World or the S&P 500 — allow your returns to compound over time through price appreciation and dividend reinvestment. When dividends are reinvested rather than withdrawn, they purchase additional shares, which themselves generate future returns. This is compounding in its most powerful form.

Retirement Savings (Provident Funds)

Many Cypriot employers offer provident funds. If you participate — and especially if your employer matches contributions — you are effectively receiving free money that also compounds over your working life. Maximise these contributions wherever possible.

Stocks

Individual stocks that pay dividends offer the same reinvestment dynamic. A company growing its earnings year after year, with reinvested dividends, delivers compounding returns over the long run.

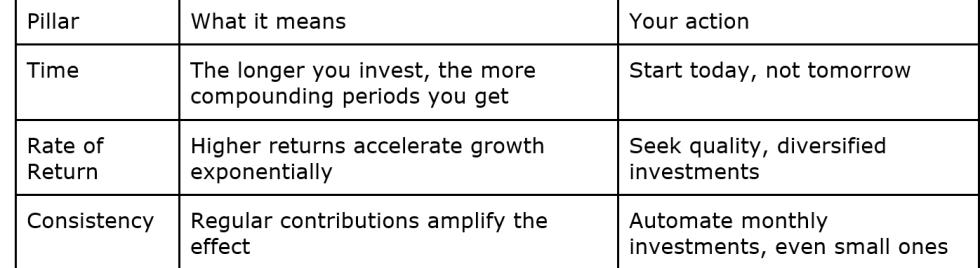

The Three Pillars of Compounding Success

Regardless of what vehicle you choose, three factors determine the magnitude of your compounding outcome:

Of these three, time is the one you can never recover. A 25-year-old who starts investing has an irreplaceable advantage over a 35-year-old — even if the latter eventually invests more money in total.

Small Numbers, Big Results

One of the most persistent myths in personal finance is that you need significant capital to start building wealth. Compounding demolishes this myth.

Consider investing just €100 per month beginning at age 25, at an average annual return of 7%:

- At age 45 (20 years): approximately €52,000;

- At age 55 (30 years): approximately €121,000;

- At age 65 (40 years): approximately €263,000

Total amount actually invested: €48,000. The rest — over €215,000 — is the pure result of compounding. Your money worked harder than you did.

This is accessible to virtually anyone. A daily coffee foregone, a monthly subscription cancelled, a small portion of a paycheck redirected — these modest choices, sustained over time, produce life-changing outcomes.

A Word on Inflation and Real Returns

No article on compounding would be complete without addressing inflation — the quiet force that erodes purchasing power over time. If your savings account pays 2% annually but inflation runs at 3%, your real return is -1%. In other words, your money is technically growing but actually losing purchasing power.

This is why simply keeping money in a low-yield savings account is not enough. For compound interest to truly work in your favour over the long term, your returns must outpace inflation. Historically, diversified equity portfolios have achieved this; cash deposits often have not.

Always think in terms of real (inflation-adjusted) returns, not just nominal ones.

The Bottom Line for the Young Cypriot Investor

Compound interest is not a secret reserved for the wealthy or the financially sophisticated. It is a mathematical certainty available to everyone — and it rewards those who start early, stay consistent, and remain patient.

The CFA Institute's foundation of financial literacy rests on one principle: informed individuals make better financial decisions. Understanding compounding means understanding that time is your most valuable financial asset — and unlike money, it cannot be earned back once it is spent.

Whether you are a recent graduate in Nicosia, a professional in Limassol, or a parent thinking about your child's future, the message is the same: the best time to start was yesterday. The second-best time is today.

Open that investment account. Set up that automatic monthly transfer. Let the snowball begin its journey down the hill. In 30 years, you will hardly remember the sacrifice — but you will absolutely feel the reward.

*Simon Kesterlian, Valuation Senior Associate @ Qfin | CFA, MSc, BSc writing as a member of the CFA Society Cyprus